Credit unions have been around for centuries, providing their members with the opportunity to join a financial institution that caters to their individual needs. Offering competitive rates and services, credit unions provide an alternative to traditional banking options. They are especially attractive to consumers who need to meet the higher standards set by larger banks.

The concept of ‘credit union’ has its roots in 19th-century Europe as a way for local people to pool resources and lend money within their community. Thousands of credit unions operate worldwide with varying levels of law depending on the region or country today. One of the main benefits offered by these institutions is the ability to make deposits in credit unions and receive competitive interest rates. Individuals access better loan terms than they find elsewhere by working together.

Key Takeaway:

Credit Unions present an attractive alternative to traditional banking options, offering opportunities for better loan terms, competitive interest rates, and the convenience of making deposits in credit unions for their members.

- Credit unions provide an alternative to traditional banking options with personalized attention and care for each member.

- Membership in credit unions is limited and open only to certain individuals or groups who share an established bond.

- Credit unions provide various essential financial services, from savings accounts and loan products to special offerings tailored toward certain needs.

- Credit unions have some drawbacks, including limited availability, stricter requirements for membership, lower interest rates on savings accounts, and limited access to products and services.

- Credit unions are community-focused institutions that offer educational resources and opportunities for members to help them make informed choices regarding managing their finances.

- Credit unions offer a variety of products and services, including loans, mortgages, home improvement financing, and business lines of credit. They generally have lower loan interest rates than traditional banks and fewer transaction fees.

What Is A Credit Union?

Credit unions act as cooperatives where members pool their money to make more loans available at competitive rates and fees. They provide members access to the same products and services as traditional banks, but with a difference, personal attention and care for each person joining their community.

Members receive benefits such as higher dividends on savings accounts, lower fees on checking accounts, better customer service, access to special products or discounts not offered by other banks, and even reward programs just for using the credit union’s services. Borrowers who join a credit union take advantage of many unique opportunities not found anywhere else in finance.

Who Can Join A Credit Union?

Membership is limited and open only to certain individuals or groups who share an established bond. This bond is often based on a field of membership that determines eligibility to join a credit union. Listed below are the criteria to join a credit union based on the field of membership.

- Must be employed by a particular company or organization.

- Live, work, worship, or attend school in a specific geographic area.

- Belong to a professional association.

- Have family ties with existing members.

- Participate in a volunteer program associated with the credit union.

It’s easy to see why many people choose credit unions over traditional banks, with their focus on member satisfaction and commitment to helping the borrowers they serve to achieve their financial well-being. Many credit unions offer low-cost loans at competitive rates. They provide benefits such as education about budgeting and saving money, youth accounts designed specifically for children, insurance products, and online banking tools.

What Kind Of Financial Services Does A Credit Union Provide?

Credit unions are community-focused banking institutions that provide financial services to their members. Most credit unions offer savings accounts with competitive interest rates that allow money to be deposited or withdrawn anytime. Members access checking accounts and debit cards, making payments securely online or in person. Many credit unions extend loans such as mortgages, auto loans, personal loans, and lines of credit for various uses. The loans come with lower interest rates than other banks due to the cooperative nature of credit unions. Some credit unions offer benefits like travel insurance, identity theft protection, and investment opportunities for those looking to grow their wealth over time.

Credit unions provide various essential financial services, from savings accounts and loan products to special offerings tailored toward certain needs. Numerous advantages are associated with joining a credit union beyond cost savings. Understanding all the options help individuals choose the best solution for their unique circumstances.

What Are The Benefits Of Joining A Credit Union?

Joining a credit union is like stepping into an exclusive club that offers its members unique benefits. Many credit unions provide specialized products and services tailored to their members’ needs. Since many credit unions are community-based organizations, they often offer educational resources and opportunities for members to help them make informed choices regarding managing their finances. One important aspect to consider is that credit unions are insured by the Federal Deposit Insurance Corporation (FDIC), which adds an extra layer of security for members.

The perks of joining a credit union are worthwhile; members save money through lower interest rates and gain access to valuable tools and resources unavailable elsewhere, including the protection provided by the Federal Deposit Insurance Corporation.

Lower Loans Rates and Fees

Lower loan rates and fees are the most obvious benefit credit unions offer. They generally provide significantly lower interest rates on loans than banks do, meaning their customers get more money for less cost. Credit unions have fewer or no costs associated with taking out a loan, such as application fees or prepayment penalties.

Reduced interest rates and minimal fees make borrowing money through a credit union attractive. Credit unions offer these reduced rates because profits from lending activities are used to improve services or paid directly to their members in dividends rather than going into corporate pockets like at banks. Credit unions charge fewer fees associated with borrowing money than traditional banking institutions, saving borrowers substantial cash in the long run.

Higher Savings Rate

Credit Unions offer a life preserver with the promise of higher savings rates. Credit unions boast higher savings rates than banks because they are member-owned financial institutions. Profits from services such as loans are returned directly to members rather than shareholders’ pockets, making fees to be lower, loan interest rates tend to be better, and investments generally have greater growth potential. They are creating an incredibly attractive alternative for those hoping to save money or make wise investments with their hard-earned cash.

Member-Owned

Credit unions are nonprofit corporations and nonprofit organizations owned by their members, and they offer services to their members that are similar to those provided by banks. The concept of a credit union is based on the principle of member ownership. The ownership structure allows credit unions to return profits to their members through higher savings rates or lower loan fees.

Members benefit from greater control over how their money is managed and invested. They have a direct say in decisions, such as setting interest rates and approving investments. They attend annual meetings where they get an overview of the financial activities of their local credit union branch. Member ownership allows individuals to participate directly in managing their finances through collective action with other members who share similar interests.

More Personal Service

The idea of ‘more personal service’ at credit unions is met with some resistance; after all, larger banks and financial institutions provide more convenience for their customers. Many customers prefer to have a relationship with an institution they are a member of, not just another client. Credit unions offer this experience, providing services tailored to each member’s needs while avoiding the hassle of dealing with large corporate entities.

Credit union membership often includes access to personalized banking products, such as checking and savings accounts, investment options, mortgages, loans, and other services. Many credit unions provide benefits such as free checking account maintenance or reduced rates on loan payments. Members enjoy greater flexibility when managing their finances and making sound decisions about money management by taking advantage of these special features. Members feel confident knowing that their interests come first because credit unions prioritize individual relationships over profit margins like those in big banks and corporations.

Credit unions are placed to help individuals develop better financial habits and make informed choices about how best to manage their money, with their focus on one-to-one customer care and attention to detail within local communities. Additionally, they impact the daily life of their members by fostering financial stability and growth.

Focus On Local Communities and Daily Life

The focus of credit unions on local communities is a key element that sets them apart from other financial institutions. Credit unions are often locally based and have strong ties to their surrounding areas, which allows them to provide services tailored to the members’ needs in those regions.

Three primary advantages become apparent as part of its emphasis on local communities.

Greater Trust

Members often experience a greater sense of trust with their credit union. Since credit unions are member-owned and operated, they tend to prioritize the needs and interests of their members over profits, fostering a strong sense of community and trust.

Accessibility

Credit unions are often more accessible due to their close proximity to the communities they serve. Members can easily access services and resources without the need for long commutes or navigating through complicated corporate structures.

Community Involvement

Credit unions are renowned for their strong focus on community outreach and involvement. They actively participate in and contribute to community development initiatives, providing support and resources to improve the well-being of the community at large.

People who join credit unions tend to feel like they are entering something bigger than just another banking platform; they become part of a larger social group with shared values and goals with all the benefits.

Credit unions bring a unique level of service not found elsewhere in the industry by emphasizing their connection to local communities. It enables customers to find comfort in knowing someone is looking out for their best interest while allowing them access to all the resources available through traditional banking systems.

Access To Financial Education

Credit unions are rooted in the principle of helping local communities, and a key part of that is providing access to financial education. Credit unions strive to guarantee their members have the information they need to make smart decisions about their finances to build wealth responsibly. Education initiatives include seminars on budgeting and saving money and courses on using credit cards wisely and understanding mortgages. Financial education programs help people become more financially literate, paving the way for them to reach their financial goals.

Many credit union branches provide one-on-one counseling services for those who want personalized advice from an expert. Individuals discuss their situation and get actionable tips for managing their money. Credit unions demonstrate their commitment to helping people with their immediate needs and equipping them with lifelong skills that benefit them long-term by offering this tailored guidance. It’s no wonder many choose credit unions over other banking institutions when seeking assistance managing money with comprehensive resources.

What Are The Drawbacks Of Joining A Credit Union?

Listed below are some of the drawbacks of joining a credit union.

- Credit unions are only sometimes available in all areas, making them inaccessible to many potential members.

- Stricter requirements. It would be best if you met certain criteria, including geographical boundaries and employer-based membership, to become a credit union member,

- Lower interest rates. Credit unions offer lower interest rates than banks on loans and mortgages, but they offer lower returns on savings accounts and other investments.

- Limited access. Credit unions are often smaller than banks, which limits the number of products and services available to members.

- Limited ATM networks. Credit unions generally have fewer ATMs in their network than banks, which is inconvenient for members who need access to cash.

Do Credit Unions Impose Stricter Requirements?

It depends on the credit union and the loan or financial product offered. It is worth contemplating the requirements they impose to become a member. It is not the case with credit unions, while traditional banks are usually more lenient regarding selection criteria. The organizations require prospective members to meet certain eligibility criteria to guarantee that only those benefitting from their services are accepted into membership.

Below are some of the most common requirements for becoming a credit union member.

- Geographical boundary Credit unions often limit membership to those who live, work, or worship in a specific area.

- Employer-based membership is a type of membership that requires one to be employed by a certain organization or company.

- Association-based membership Members join associations affiliated with certain credit unions.

- Family-based membership Some credit unions allow family members of existing members to join.

It is necessary for people looking at becoming members of a credit union to research its exact requirements before applying. The knowledge helps individuals assess if they are likely candidates for acceptance by the particular credit union they wish to join. Understanding what is expected enables them to make better decisions if being part of this kind of institution is right for them to meet their needs and goals, such as obtaining business loans.

Potential applicants decide how best to proceed toward financial stability and security through membership in a credit union. Researching the various aspects of credit unions is thoroughly worthwhile in making informed choices about money management strategies. Exploring product diversity offered by credit unions, including business loans, offers another avenue of investigation.

Credit Unions And Product Diversity

Credit unions have become increasingly popular in the 21st century due to their various benefits and services, such as business loans. Listed below are some of the advantages of using a credit union.

- Better Loan Rates Credit unions offer lower interest rates on loans than traditional banking institutions, as they must satisfy their shareholders rather than generate profits for investors.

- Generous Rewards Programs Credit unions often provide more generous rewards programs than banks, offering benefits such as cashback on purchases, free checking accounts, or discounted insurance policies.

- Fewer Transaction Fees Credit unions usually have fewer transaction fees than other banking options, making them less expensive for customers.

- Impressive Product Diversity Credit unions offer various financial products and services, including mortgages, car loans, home improvement financing, business lines of credit, and more.

Listed below are some drawbacks to using a credit union.

- Slower Cash Access Credit unions often need more physical branches and ATMs nationwide, leading to slower customer access.

- Third-Party Network Dependence Customers can only make withdrawals or deposits by relying on third-party networks, leading to delays and higher fees in certain circumstances.

Using a credit union depends on the consumer’s comfort level and financial needs.

Here is a table highlighting key differences between credit unions and traditional banks.

| Factors | Credit Unions | Traditional Banks |

|---|---|---|

| Ownership | Member-Owned | Investor-Owned |

| Loan Rates | Lower | Higher |

| Rewards | Generous | Limited |

| Fees | Fewer | More |

| Products | Diverse | Standard |

| Cash Access | Slower | Faster |

The table shows that credit unions have unique advantages over traditional banks, such as lower loan rates and more generous rewards programs but have some drawbacks, such as slower cash access. It is necessary to consider your financial needs and preferences carefully before deciding whether to use a credit union or a traditional bank.

Slower Access To Cash

Cash access is an essential component of credit union services, but it often comes at a slower rate than what is expected from other financial institutions. Credit unions need more resources than larger banks regarding online banking options and automated teller machines (ATMs). Credit unions need more capital to meet high-volume customer needs because many credit unions are locally focused on smaller memberships and loan limits.

Customers who prefer quick transfers and withdrawals wait for more funds due to limited availability or processing times. Customers must incur fees associated with faster payment methods offered by third parties or other traditional banking institutions to get funds immediately. All factors contribute to slower access to cash through credit unions than today’s financial options.

Lower Loan Limits

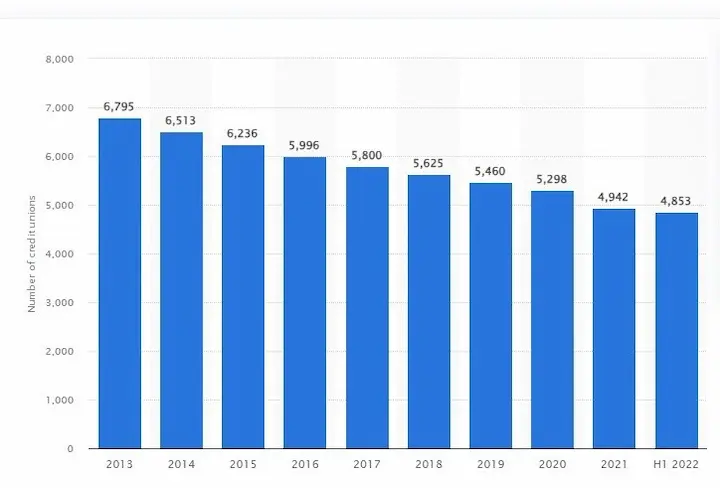

Credit unions are a great alternative to banks, offering many advantages. One interesting statistic is that at least 80 million Americans are members of credit unions, according to the National Credit Union Association (NCUA).

Their loan limits are often lower than traditional banks. According to data from the National Credit Union Administration, the median loan limit for credit unions in the US is $35,000.

Here is a table summarizing the loan limits for credit unions.

| Loan Type | Median Loan Limit (December 2021) |

|---|---|

| Credit Card | $20,000 |

| Auto | $30,000 |

| Personal | $15,000 |

| Mortgage | $400,000 |

It is worth noting that credit union loan limits vary by institution and location, so it is necessary to check with your local credit union for specific information on loan limits. Credit unions remain an excellent choice for consumers looking for affordable financing options despite the lower loan limits.

Listed below are the benefits of credit unions compared to traditional banks.

- Lower Rates. Credit union loans tend to have lower interest rates than bank loans due to their not-for-profit nature. There are significant savings if you borrow large amounts or take out multiple loans.

- More Flexible Terms. Most credit unions allow borrowers more flexibility regarding loan terms. Most credit unions provide personalized service, and borrowers get tailored advice for their financial needs.

- Greater Accessibility. Unlike traditional banks, most credit unions do not impose such restrictions on their members, often requiring high minimum balances and other fees. It is easier for them to access and use than other financial institutions, even those without good credit scores.

They remain attractive when looking for competitively priced financing options since they provide better terms than conventional lenders and greater Accessibility and convenience for users. At the same time, there are some limitations concerning loan amount limits at US credit unions.

Credit Union Vs. Banks: A Comparison

The great debate between credit unions and banks continues to this day, with both sides arguing their points of view. It is a battle of ideals, where one side seeks to provide services that benefit the community while the other strives to make profits for shareholders.

Credit unions have lower loan limits than most banks. They offer more competitive rates on savings accounts and loans. Members receive better service from credit unions due to their smaller size and local operations, allowing them greater flexibility when dealing with customers’ needs. They are often seen as more customer-focused than traditional banking institutions because they are committed to providing financial education and advice rather than focusing solely on profit margins.

It is clear that when choosing between a bank or a credit union, there is no right or wrong answer, as each has its advantages and disadvantages depending on individual circumstances. What matters most is understanding the differences to make an informed decision based on personal priorities such as interest rate preferences, customer service levels, access requirements, or any other factors needed to achieve financial success.

Final Thoughts

Choosing between a credit union and a traditional banking institution takes time and effort. Credit unions offer lower loan rates, fees, and limits than banks but have slower access to cash. Consumers need to weigh each option’s pros and cons before deciding.

Credit unions allow people to take control of their financial future. Members can craft a path toward fiscal responsibility by utilizing products tailored specifically to them with competitive interest rates, flexible repayment options, and more personalized customer service.

Credit unions must be considered when deciding which financial institution to use. They provide many benefits that save money in the long run while providing customized services designed to customers’ needs. Individuals find the best fit for their situation to make sound decisions about their finances by carefully researching both options.

Frequently Asked Questions

What is a credit union, and how does it differ from a traditional bank?

A credit union is a nonprofit financial cooperative owned by its members. Unlike banks, they return profits to members in the form of better rates and fees. Membership eligibility is a key difference from banks that are open to anyone.

What are the key benefits of joining a credit union compared to a commercial bank?

Benefits include higher interest rates on savings, lower rates on loans, much lower or no fees, personalized service, investment in the community, and democratic governance by the members. Credit unions cater directly to customers, not shareholders.

What are the potential drawbacks or limitations of using a credit union for financial services?

Drawbacks include smaller branch networks, limited geographic reach, fewer technology options compared to mega banks, narrower arrays of financial products, and membership eligibility restrictions in some cases.

Can anyone join a credit union, or are there specific eligibility criteria that need to be met?

Each credit union sets its own field of membership criteria. Most base eligibility on factors like employer, location, association membership, or family. Individuals cannot join any credit union they want but there is likely one for which they qualify.

How do credit unions typically offer competitive interest rates and lower fees compared to banks, and what are some examples of financial products they provide to their members?

Credit unions pass earnings back to members, not stockholders. Products include free checking, high-yield savings, certificates of deposit, auto loans, mortgages, credit cards, bill pay, mobile banking, and financial advice services.