How Exactly Do PaydayChampion Payday Loans Work?

Are they beginning a vicious cycle of high-interest payments and expensive fees?

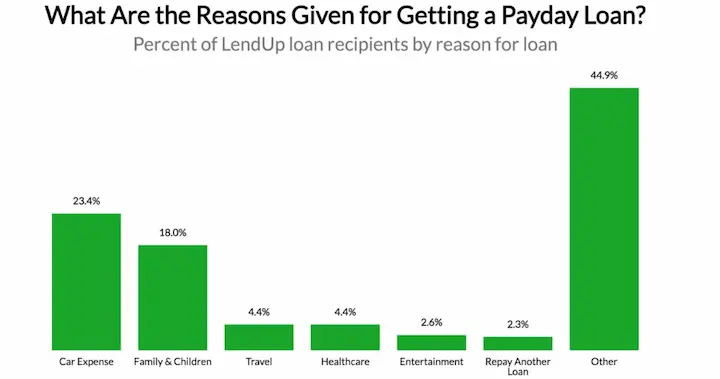

When you are in financial trouble, and your credit score is not good, or you have bad credit, searching for quick solutions like payday loan services can be tempting. Although PaydayChampion payday loans near me work straightforwardly, they can be expensive sometimes. Expect additional finance charges if you miss your monthly payments, leading to a debt trap for some individuals.

The Consumer Financial Protection Bureau (CFPB) reports that nearly 25% of payday borrowers default on repayment terms, and more than 80% need to borrow again within 14 days, affecting their financial situation.

What is a PaydayChampion Payday Loan?

A PaydayChampion Payday Loan is a short-term unsecured loan designed for individuals with varying credit histories. This type of Payday Lending offers borrowers an alternative solution when in need of quick cash. However, it is essential to be cautious, as the annual interest rate on these loans can be high. You should explore a payday alternative to avoid getting caught in a cycle of high-interest payments and expensive fees.

Payday loans are short-term consumer loans that last for up to two weeks. You can write a check or provide a debit number to receive the cash and credit union the same day.

Among various forms of credit, online payday lenders will cash the check when the due date has passed to complete the loan in a storefront payday lender. You can arrange to pay the loan back at the office if you have the cash. Financial experts consider these loans unsecured, and their lenders charge high-interest rates and default fees since these immediate cash needs require no credit check or other security.

Online payday loans may incur higher costs than anticipated, including late payment penalty fees.

At PaydayChampion, we take pride in our nationwide presence and commitment to providing reliable financial solutions to needy individuals. With a strong focus on payday loans, we have established ourselves as a trusted resource for short-term lending assistance. As part of our dedication to accessibility, we are actively operating in numerous American states, offering our services to residents across the country. To showcase our extensive reach and reinforce our commitment to serving customers, we have compiled a comprehensive table below, highlighting all the states where our company is active. Whether you are facing unexpected expenses or need quick access to funds, we are here to assist you in navigating your financial challenges, with our presence spanning multiple states and our unwavering dedication to your financial well-being. Explore the table below to discover the states where we are ready to support you in your payday loan needs.

| Alabama (AL) | Alaska (AK) | Arizona (AZ) | Arkansas (AR) |

| California (CA) | Colorado (CO) | Connecticut (CT) | Delaware (DE) |

| District Of Columbia (DC) | Florida (FL) | Georgia (GA) | Hawaii (HI) |

| Idaho (ID) | Illinois (IL) | Indiana (IN) | Iowa (IA) |

| Kansas (KS) | Kentucky (KY) | Louisiana (LA) | Maine (ME) |

| Maryland (MD) | Massachusetts (MA) | Michigan (MI) | Minnesota (MN) |

| Mississippi (MS) | Missouri (MO) | Montana (MT) | Nebraska (NE) |

| Nevada (NV) | New Hampshire (NH) | New Jersey (NJ) | New Mexico (NM) |

| New York (NY) | North Carolina (NC) | North Dakota (ND) | Ohio (OH) |

| Oklahoma (OK) | Oregon (OR) | Pennsylvania (PA) | Rhode Island (RI) |

| South Carolina (SC) | South Dakota (SD) | Tennessee (TN) | Texas (TX) |

| Utah (UT) | Vermont (VT) | Virginia (VA) | Washington (WA) |

| West Virginia (WV) | Wisconsin (WI) | Wyoming (WY) |

What Happens if I Cannot Pay My Payday Loan on Time?

You must pay your payday loan from PaydayChampion on time to avoid being charged late payment fees and interest. Depending on the state where you reside, it is likely that your loan could become delinquent if payments are not made according to your agreed-upon schedule. In such cases, a collection agency or debt collectors may get involved, and you may face a more extended repayment period for your loan, making the debt payment more challenging.

Online lenders may take further collection actions, such as filing an official legal complaint against you to obtain payment. Debt collection agencies can be involved if the situation becomes severe. Making your scheduled payments on time is important to avoid these potential consequences.

If you need to pay back a payday loan quickly enough, your lender might offer to extend the amount of time that it loans you. This is referred to as rollover loans.

Suppose you have $200 to pay for a car, medical bill, or other expenses that can’tcan’t wait. Your lender might agree to extend that $200 for another two weeks, making the amount due $480.

If you cannot repay the original loan when it is due again, your lender may offer another extension and increase the time it loans you. The rollover can continue until the emergency loan bad credit has been rolled over several times, resulting in an extremely high-interest rate on your outstanding balance.

Are There Better Options Than a PaydayChampion Payday Advance?

Yes, there are various types of loans available for borrowers. Some options include credit card advances, auto loans, and alternative loans from institutions other than mainstream and traditional banks. Many people also turn to pawn shops for quick cash or seek different loan options from the payday industry.

To determine which loan option is right for you, it’s essential to understand the basic loan process and review your bank statements to evaluate your financial situation. This will help you find the most suitable solution to your monetary needs and avoid unmanageable debt.

Yes, there are better options than a PaydayChampion payday advance. Banks offer installment loans as an alternative, which typically have lower interest rates. However, the application process for traditional loans can be more strict, often requiring proof of monthly income and a decent credit score. In addition, a traditional deposit bank account might be necessary.

If you have a low credit score, look for lenders offering bad credit loan payday. Borrowing alternatives like this one has fewer restrictions. Online borrowers only need to present documents, such as a source of income, to prove they can afford the monthly payments. Some lenders may also offer a prepaid card as an alternative to a bank account.

Cash advance loans online are easy to acquire, but you must be careful. Many lenders offer a predatory loan that has exorbitant annual percentage rates. This can greatly increase the cost loan and lead to significant debt. Make sure to research the average interest rate for such loans.

You should shop for the best cash advance loan interest rates and terms if you need money to pay for unexpected emergencies. Small-dollar loan lenders can charge you high interest and fees, as you have seen. Compare options like a loan in person from a local lender and consider loan maximums for your needs.

Some lenders might require a personal check or an additional finance charge for their services. Make sure to read the terms and conditions before borrowing.

Tips for Payday Loan Borrowers

Avoid taking on debt you cannot manage when seeking quick cash solutions. Always borrow responsibly and explore your options before deciding on a payday loan. Ensure you understand all terms and conditions before committing to a loan, including repayment schedules, interest rates, and associated fees. Also, find a loan with direct access to funds, which can help you get the money you need faster.

Knowing how to get the best out of your Direct payday or personal loans is necessary to avoid predatory lending.

For example, you should be aware that the non-sufficient fund’s fees (NSF) can quickly add up if you have multiple transactions, can soon add up. You can link your savings account with your checking to cover accidental overdrafts. Also, take note of check fees and post-dated check regulations, as these can impact your finances.

A portion of your direct deposit and loans work payday can be automatically transferred to an account with the aid of credit bureaus. Moreover, set up an automatic transfer to help you build your savings and remember to add money to your emergency fund. Remember federal regulations, rate caps, and shorter terms when selecting payday loans.

PaydayChampion makes it easy to automate your savings with our Round Up to Save Program. We automatically transfer any difference to your account when you purchase your debit card. It includes a cash advance until you pay back the initial loan with the initial loan amount to avoid the payday loan trap. We match up to $250 of your savings at the end in financial services.

As an average borrower, it’s essential to be well-informed and careful when dealing with loan providers. Compare traditional, alternative, and comparison lenders to ensure you get the best deal. Understand the employment verification requirements and specific terms of auto title loans before opting for them.

Finally, you should always read the terms and conditions of your loan before signing. PaydayChampion provides a detailed explanation of all our loan terms and conditions so you can make an informed decision.

Here are some statistics about traditional, alternative, and comparison lenders:

| Type of Lender | Market Share | Loan Amounts | Interest Rates |

|---|---|---|---|

| Traditional Lenders | 80% | Larger | Lower |

| Alternative Lenders | 20% | Smaller | Higher |

| Comparison Lenders | Small | Similar to Traditional Lenders | Similar to Traditional Lenders |

The Bottom Line

Payday loans can be a quick and easy way to get cash when needed, but they can also be expensive. Banks offer alternatives to payday loans, such as installment loans with average loan-size interest rates. Online lenders may offer less restrictive direct loans but charge high interest and fees. It’sIt’s important to understand the terms and conditions of your loan before signing.

Shopping for the best cash advance loan interest rates and terms is important. You can also set up an automatic transfer to help you build your savings and avoid forgetting to add money to your emergency fund. Finally, always read the terms and conditions of your loan before signing.

In recent years, there have been actions against payday lenders, and the Federal Register has taken notice. This has pushed for alternative lending options like Credit Unions and Small Loan Companies. Unfortunately, many people, especially those of Hispanic descent, still lack access to these options. To address this issue, experts have released a white paper examining the impact of such loans on financially vulnerable communities.

As a borrower, weighing the pros and cons and exploring alternative loan sources if needed is crucial. It’sIt’s worth noting that ads for payday loans are often misleading, enticing borrowers to apply for a $100 one-week loan without considering its true cost. Payday lenders and auto pawn loans are equally more expensive than traditional lending sources.

Frequently Asked Questions

What is a payday loan, and how does it work?

A payday loan provides a short-term cash advance using a post-dated check or electronic withdrawal as collateral. Full repayment is typically due within 14 days or by the borrower’s next pay date. High fees and interest rates apply.

What are the key features and requirements of a payday loan?

Payday loans feature high costs, short repayment terms of 2-4 weeks, no credit check, fast approval, collateral like a check or ACH authorization, and access to cash within 24 hours in many cases.

What are the pros and cons of using payday loans for short-term financial needs?

Pros are quick cash access and high approval rates. Cons are extremely high fees and interest rates over 300% APR, short repayment timelines, and the risk of getting caught in cycles of new debt. They should be a last resort option.

How much can I borrow through a payday loan, and what are the associated fees and interest rates?

Loan amounts are typically $100-$1000 based on state laws. Fees range from $10-$30 per $100 borrowed. APR interest rates average 400% but can exceed 600% in some cases.

What are the potential risks and alternatives to consider before getting a payday loan?

Risks include high costs, debt cycles, damaged credit if unpaid, and potential collection harassment. Safer alternatives are credit cards, employer or family loans, credit union loans, crowdfunding, or government assistance.