Life is like a financial roller coaster where one moment you feel secure, and the next you struggle to make ends meet. Credit limits are designed to know that people stay within an acceptable range of spending power, but it is not enough. Access to more capital in times of need provides peace of mind when finances become tight. Increasing credit limits is taking steps towards greater financial freedom, climbing higher on the metaphorical ladder, and reaching closer to economic security. Individuals gain insight into slowly ascending the ladder, carefully planning each step to avoid missteps or falls.

Financial literacy is necessary to reach their goals and aspirations without getting weighed down by debt or other money-related issues. Understanding how to increase your credit limit is just another piece of knowledge that help lead individuals closer to achieving proper economic stability throughout life. The following sections explore how one raises their line of credit to access funds whenever needed.

SUMMARY

- Credit limits serve as a protection mechanism for borrowers and lenders by preventing overextension of borrowing capacity and encouraging responsible lending practices.

- Understanding how credit limits work helps individuals manage their debts responsibly, make informed decisions about their finances, and manage their finances successfully.

- Income level, payment history, and current financial obligations impact an individual’s credit limit. Lenders offer special promotions or rewards programs that temporarily or permanently increase one’s available credit limit.

- Increasing credit limits through strategies such as improving credit scores, becoming an authorized user, and applying for a new card.

- Proven strategies to demonstrate creditworthiness include establishing a good payment record, utilizing multiple forms of credit, limiting borrowing relative to income, and applying for types of credit cards.

- Individuals successfully increase their credit limit, manage their debts responsibly, and achieve proper economic stability throughout life.

What Is A Credit Limit?

Credit limits refer to the maximum amount of money an individual can borrow from their lender. The limitation helps protect borrowers and lenders by reducing debt levels, preventing overextending borrowing capacity, and encouraging responsible lending practices.

Credit limits vary greatly depending on income level, credit score, payment history, current financial obligations, etc. People with higher incomes and better credit scores can access more generous credit limits. Other lenders offer special promotions or rewards programs that temporarily or permanently increase one’s available credit limit.

Understanding a credit limit provides valuable insight into why the restriction exists and how it affects an individual’s ability to borrow money successfully. Individuals can make informed decisions regarding their finances and responsibly manage their debts with the proper knowledge about how income level and other financial commitments impact their overall borrowing capacity.

How Does A Credit Limit Work?

The maximum amount of money charged to a particular line of credit is the credit limit. The credit limit feature helps keep borrowers from overspending and getting into unmanageable debt. It works by setting an upper limit on how much debt you have about your available credit.

Your creditor assesses your financial situation and what credit limit is extended. Higher limits go to people with better income levels or established histories of responsible payment practices. The lender looks at other factors when deciding your individualized limits, such as employment history, type of collateral offered, and current economic conditions at the time of application.

It’s necessary to understand how your credit limit works so you don’t exceed it and accrue costly late fees or damage your overall credit score due to missed payments or overextended accounts. Knowing the information is necessary if you plan on applying for any loans or lines of credit since exceeding a pre-established limit lower your chances for approval.

What are the Ways To Increase Your Credit Limit?

To keep your finances in order and achieve goals increasing your credit limit is necessary to keep your finances in order and achieve goals. The ways to increase your credit limit include improving your credit score, getting added as an authorized user, and applying for a new card.

There are several ways to increase your credit limit.

- Improve Your Credit Score.

Improving your credit score is one way to demonstrate sound financial responsibility and show potential lenders you take on debt without defaulting or missing payments. Pay down existing debts, avoid late payments, and dispute any errors on your report if necessary. - Get Added As an Authorized User.

Becoming an authorized user is another option if you need more history or access to higher limits. It involves ensuring the person adding you has excellent credit, pays their bills on time every month, and agrees not to use yours unless expressly permitted by both parties. - Apply For A New Card.

Applying for a new card works if you need more than the previous two options to be feasible, temporarily lowering your overall score until you drop off after two years. Know there aren’t any hidden fees associated with the card before applying, such as annual charges or balance transfer fees which negate any potential benefit from increased spending capacity.

What are the Proven Strategies To Demonstrate Creditworthiness?

Proven strategies to demonstrate creditworthiness are necessary to effectively increase one’s credit limit. The first and foremost strategy involves establishing a good payment record by paying all bills on time which reflects positively on a person’s financial standing and enables individuals to access higher credit levels.

Utilizing multiple forms of credit, such as debit cards, installment loans, and lines of credit, shows creditors that borrowers responsibly manage their finances. Individuals must strive to keep their debt-to-income ratio low by limiting their borrowing relative to what a person makes annually or monthly. Applying for other types of credit cards from different lenders helps build up an individual’s available line of credit.

The proven strategies demonstrate one’s credibility and help create a positive impression about an individual when seeking out sources of financing. Anyone substantially increases their limits with the right approach and dedication.

Increasing Your Income

Increasing your income is like a farmer planting seeds of abundance in his field. It involves taking intentional action toward harvesting more financial resources, which helps you increase your credit limit. Here are three ways to do it.

Negotiate Raises or Bonuses

Research what others in similar roles earn and use that information when negotiating for higher pay with your employer.

Explore Additional Income Sources

Get creative about other sources of income. Do freelancing on the side, start an online business, rent out space in your home or vehicle, look into passive income opportunities, or apply for part-time jobs to boost your overall earnings.

Assess Other Expenses

Cut back on unnecessary spending and allocate the saved funds towards growing bigger than yourself.

You demonstrate increased responsibility over finances and provide evidence of trustworthiness toward creditors by increasing income through strategies that build credibility and boost confidence in loan officers deciding if to offer more extensive lines of credit.

Keeping Your Account In Good Standing

Individuals increase their credit limit by taking proactive steps to maintain a solid financial profile. Keeping an account in good standing must be viewed as more than paying bills on time which involves building and sustaining a healthy relationship with lenders.

The optimal use of available credit is necessary for successful account management. Simple measures like tracking spending habits, budgeting responsibly, and avoiding unnecessary fees improve loan terms. The steps influence lenders to offer higher borrowing amounts or access to special rates. Staying informed about changes to existing accounts or updates on industry-wide practices helps avoid potential problems before becoming severe.

The strategies demonstrate commitment to proper fiscal stewardship, yielding greater borrowing power when looking at future loans or lines of credit. It’s necessary to know that while increasing income levels has merits, maintaining a sound payment history is necessary to improve overall financial health.

Getting A New Credit Card

Obtaining a new credit card to increase one’s credit limit is an attractive theory. It is necessary to weigh all associated costs and risks before making any financial decisions, as it affects people’s financial well-being in the long run.

Different cards have different features and benefits, so researching is necessary to determine if a new card improves your current situation or puts you into debt. Having multiple cards help build your credit score by increasing utilization with no extra spending.

Maintaining Low Credit Utilization

Maintaining low credit utilization is necessary to increase your credit limit. An example is an individual living on a fixed budget and using the existing card regularly for everyday purchases such as groceries or car payments. The approach helps maintain and improve the individual’s credit score over time with responsible use and timely payment of bills.

Listed below are the three ways how to maintain a low credit utilization.

- Budgeting and Tracking.

Creating a budget and tracking spending habits provide insights into where the money goes and identify areas where funds are saved to pay off current debt quickly. One must clearly understand their financial health by budgeting and tracking. - Making Multiple Payments throughout the Month.

Paying multiple times during the month rather than waiting until the due date reduces overall balance usage, which helps keep credit utilization at its lowest rate. - Re-evaluating Credit Card Limits.

Another way to control total balances owed is by requesting temporary increases in established limits when needed. Doing so allows individuals to maintain lower debt levels without sacrificing liquidity or access to other available resources if necessary.

Maintaining low credit utilization increases an individual’s ability to access higher lines of credit while improving overall financial health through better management strategies. Implementing the measures consistently over time makes more favorable terms from lenders, including higher limits and reduced interest rates.

Using Your Existing Card Regularly

Regularly using an existing credit card is a great way to increase one’s credit limit. It helps build trust with the lender, showing that the borrower is trusted to pay back their debt on time. It allows borrowers to show lenders that borrowers are responsible and capable of managing their finances which results in higher limits.

Regularly using an existing credit card has many benefits, too, such as helping to improve payment history and increasing available funds for large purchases or emergencies. The method provides numerous advantages regarding increasing credit limits and overall financial stability. Making consistent payments while utilizing an established line of credit is smart.

Consolidating Credit Card Debt

Consolidating credit card debt is one way to increase your available credit limit. It helps free up more money used for other purposes and makes it less likely you exceed your current credit limit. Transferring multiple accounts with high balances into a single low-interest loan significantly reduces the interest paid on debts over time, providing enough wiggle room in your budget to allow for an increased spending limit on your existing card or another new card issued by the same lender. Consolidating credit cards simplifies monthly budgeting and makes tracking progress toward eliminating debt easier.

TIP: Discuss consolidation options with a financial advisor before committing to any specific plan. A financial advisor advises you on which route suits your circumstances and goals best.

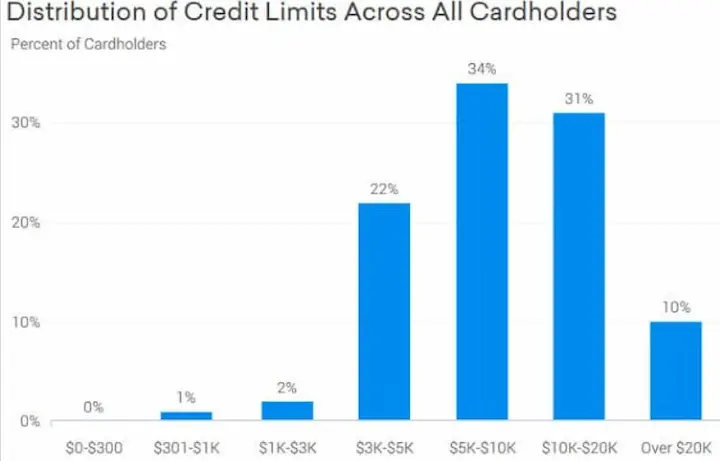

What is the Average Credit Limit?

The average American had access to $30,233 in credit across all their credit cards in 2021, according to Experian. The average credit card balance was $5,221, below the average credit limit. The average credit limit fell 1.9 percent compared with 2020 ($30,817) and 3.9 percent compared with the pre-pandemic year 2019 ($31,459).

| Year | Average Credit Limit | Average Credit Card Balance | Credit Available |

| 2021 | $30,233 | $5,221 | $25,012 |

| 2020 | $30,817 | $5,548 | $25,269 |

| 2019 | $31,459 | $6,194 | $25,265 |

The table provides a snapshot of Americans’ credit card usage trends, highlighting the credit available and changes in the average credit limit and credit card balance over the years.

Conclusion

Lenders use credit limits to prevent borrowers from overextending their borrowing capacity and to encourage responsible lending practices. Understanding how credit limits work is necessary to managing debts responsibly, and individuals can take steps to increase their limits. The steps include improving their credit score, becoming an authorized user, or applying for a new credit card.

Strategies to demonstrate creditworthiness, such as establishing a good payment record, utilizing multiple forms of credit, keeping the debt-to-income ratio low, and applying for types of credit cards, are necessary for increasing credit limits. Increasing income help increase credit limits, giving individuals more access to funds in times of need.

Frequently Asked Questions

What are the steps to request a credit limit increase on my credit card?

Call the customer service number and ask to speak with a representative about requesting a credit limit increase. Be prepared to provide your account information and income details. The rep will submit the request, which is then evaluated based on factors like your payment history.

How does a higher credit limit benefit my financial situation and credit score?

A higher limit can improve your credit utilization ratio which helps boost your credit score. It provides more flexibility in spending and allows you to make large essential purchases while staying under 30% of your total limit.

What factors do credit card companies consider when deciding whether to raise my credit limit?

Key factors are your payment history on the card, total credit utilization, income stability, credit score, and length of credit history. Low balances and on-time payments help demonstrate you can responsibly manage more available credit.

Are there any potential risks or downsides to requesting a credit limit increase?

Risks include taking on more available debt which could lead to overspending and higher balances. It may also trigger a hard inquiry on your credit report, temporarily lowering your score. However, responsible use of the higher limit can mitigate these risks.

Can you provide tips for effectively managing a higher credit limit to avoid overspending and debt?

Tips include avoiding unnecessary purchases, paying your balance in full each month, tracking spending carefully against your budget, setting text or email alerts for high balances, and applying extra payments to principal to avoid interest charges.